After a generation of steadily increasing incomes, Canadians entering the labour force after the turn of the century must cope with greater uncertainty of their future incomes, including actual drops.

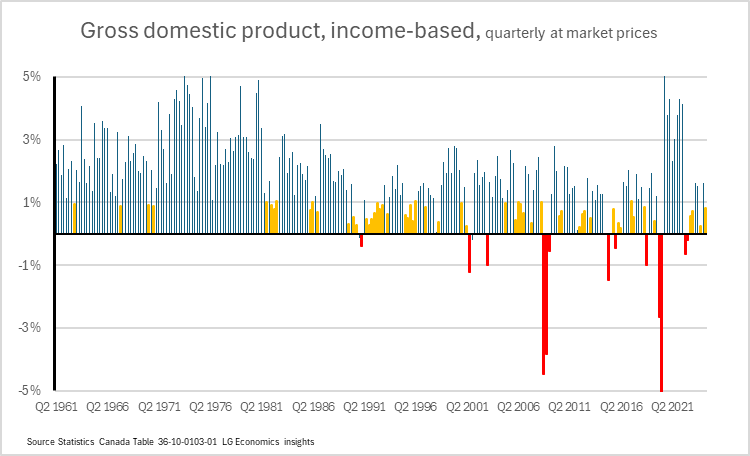

Over forty years, from 1961 to 2001, the Canadian economy generated steadily increasing incomes with the sole exception of 1991. And 1991 was a “managed” economic slowdown by the Bank of Canada to cool the economy and fight inflation. Since 2001 there have been at least 6 episodes of falling gross income: 9-11 and its aftermath, the global financial crisis, the stuttering economic recovery in 2015 and 2018, then the global covid-19 pandemic.

This post focuses on the total incomes generated by the Canadian economy. Gross Domestic Product can be determined by either of two methods that result in equivalent estimates – either summing all incomes earned within the economy (GDP income based) or by summing all expenditures made within the economy over the same period of time (GDP – expenditure based). This post focuses on the income-based approach.

Incomes include income to labour and profits to capital. Returns to small unincorporated business are measured as “mixed income”, mixed because labour income earned by the business owner and profits earned by the capital invested in the business enterprise are not recorded separately. The return to “land”, that is the economic rent associated natural resources, is not identified as a separate item in the national accounting framework.

Figure 1 shows quarterly income-based GDP performance at annualized rates. Growth over 1 per cent coloured as black, slow downs with growth between zero and one per cent are in yellow and negative growth are coded as red bars. Until 2001 quarterly economic growth was positive although slowing growth rates were becoming more frequent during the 1990’s. With the new millennium every thing changed,

Wars, financial crisis’s and epidemics were present between 1961 and 2001 but not with the virulence and frequency of the first quarter of the twenty-first century. The relative calm of the last forty years of the twentieth century may have led to certain complacency in the western economies such that the volatility of the first quarter of the this century may have unanchored confidence in the inevitable increase of economic fortunes.

Modern economies are driven by consumers and the increased uncertainty of income growth has introduced increased consumer caution, resulting in greater cautionary spending (more savings, less conspicuous consumption) dampening economic growth.

Leave a comment