Part 1 of this post focused on the level of central government debt, Part 2 focuses on the change of the level of debt. Principle factors influencing the sustainability of changes of the debt are the relationship between the real interest rate on the debt (its carrying cost) and changes in the real GDP (the tax/revenue base). Note: the health of the economy will be a factor even if the government chooses to finance the change in debt by borrowing the money instead of raising taxes.

The basic dynamic is if real GDP grows faster than the real rate of interest, then the economy can support a higher quantity of debt because the debt to GDP ratio goes down. And visa versa.

The real, after inflation interest rate, is set in the open market through the sale of American Treasury Inflation Protected Securities (TIPS). TIPS rates are published for 5, 10 and 20 year terms. The principle value on a TIPS security is tied to the consumer price index (so it retains its “real”, inflation adjusted value) and pays the TIPS interest rate on top of the CPI adjustment.

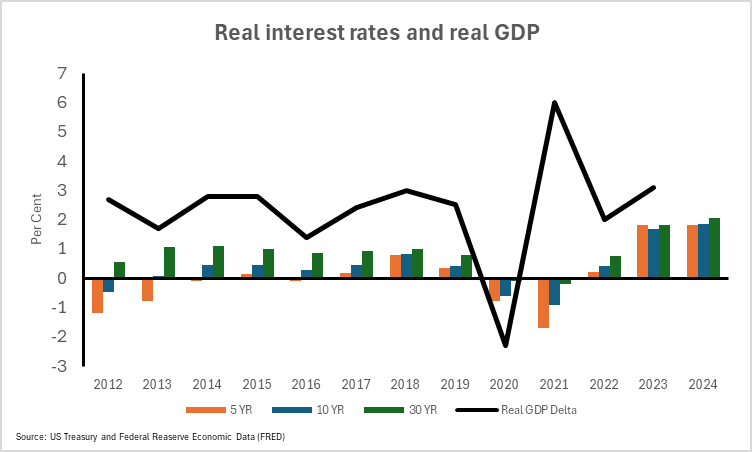

As illustrated in the figure below between 2012 and 2019 real GDP was running about 2 per centage points above the real interest rate then in 2020, the beginning of the pandemic economic shut down, real GDP fell almost 2 per centage points below real interest rates but then rebounded almost 7 per centage points above real interest rates the next year. Investors prefer a stable investment environment, with low risk and low uncertainty. That was not the investment climate in 2021. In the last two years real interests rates have shot up dramatically.

Here is the spreadsheet.

From ChatGPT:

When the real GDP grows faster than the real interest rate, several effects on the deficit can occur:

- Increased Tax Revenue: A faster-growing economy generally generates more tax revenue for the government. As businesses expand and individuals earn more income, tax collections, such as income taxes and corporate taxes, increase. This can help reduce the budget deficit as the government receives more revenue without having to raise tax rates.

- Reduced Need for Welfare Spending: With a stronger economy, there may be fewer people relying on government assistance programs such as unemployment benefits or food stamps. This reduction in welfare spending can also contribute to narrowing the budget deficit.

- Increased Economic Activity: When the real GDP grows faster, it often signifies increased economic activity, including higher levels of consumption and investment. This can lead to higher sales tax revenue and corporate profits, further boosting government income.

- Decreased Need for Fiscal Stimulus: In some cases, a rapidly growing economy may require less fiscal stimulus from the government to support economic growth. As businesses thrive and unemployment rates fall, there may be less need for government spending to stimulate demand, which can help mitigate deficit spending.

- Interest Payments on Debt: If the real interest rate remains low despite the GDP growth, the government’s interest payments on its debt may not increase significantly. This can help prevent a substantial increase in deficit spending related to servicing the national debt.

Overall, if real GDP growth outpaces the real interest rate, it can have a positive impact on the budget deficit by boosting government revenue, reducing spending needs, and potentially lowering the cost of servicing the debt. However, other factors such as government policy decisions, international economic conditions, and the overall structure of the economy will also influence the deficit outcome.

Leave a comment